Model portfolios like those I recommend are ideal for investors who have a single RRSP account. But life isn’t so simple once you’ve accumulated a significant portfolio: chances are you’ll be managing two or three accounts, and if you have a spouse there may well be a few more.

In most cases, it’s most efficient to consider both partners’ retirement accounts as a single large portfolio. In other words, there’s no my money and my spouse’s money: there’s only our money. This strategy has a couple of advantages: first, it allows the family to make the most tax-efficient asset location decisions. Second, it keeps the overall number of holdings to a minimum, which reduces transaction costs and complexity.

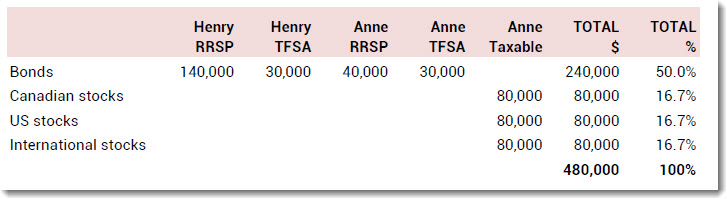

Meet Henry and Anne, who have a combined portfolio of $480,000. Let’s assume they are the same age and plan to retire at about the same time. Their financial plan revealed that a mix of 50% bonds and 50% stocks is suitable for their risk tolerance and goals. Anne has a generous defined benefit pension plan and therefore has little RRSP room: most of her personal savings go to a non-registered account. Henry has no pension plan and makes regular RRSP contributions.

If we treat all their accounts as a single portfolio, here’s how one might set it up for maximum efficiency:

With this setup, all of the bonds are in tax-sheltered accounts and the equities are in Anne’s non-registered account, which is likely to result in a lower tax bill. Moreover, the whole portfolio can be built with just seven holdings (six if they use an ETF that combines US and international equities). Nice and tidy.

Keeping it in balance

But there are potential problems here. For starters, if Henry and Anne view their accounts separately, they’ll notice his accounts are 100% bonds, while hers are over 77% equities. Although the overall mix is a balanced 50-50, the individual spouses are taking dramatically different levels of risk. This is purely behavioral, and there’s no need to make any changes if Henry and Anne are comfortable, but it’s an issue that frequently comes up with couples.

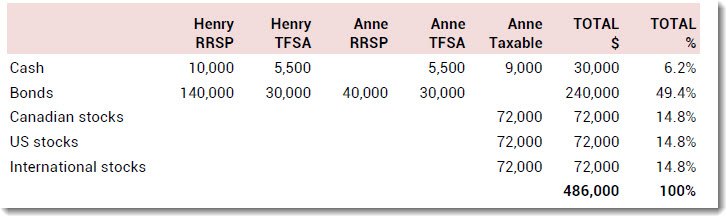

More daunting problems can arise when it’s time to add new money and rebalance the portfolio. Fast-forward a year and assume stocks have fallen in value by 10%. We’ll also imagine that Henry and Anna have made their TFSA contributions for the year, Henry has put $10,000 in his RRSP and Anne has added $9,000 to her non-registered account. Now the portfolio looks like this:

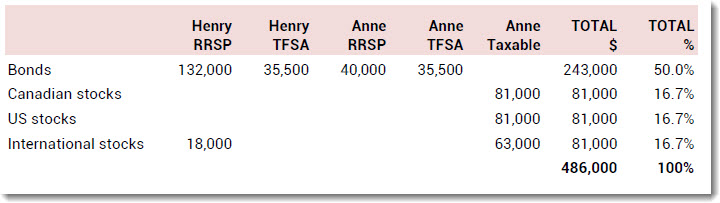

We need to rebalance to get back to the 50-50 target, but we can’t do that by simply adding to the existing holdings. The equity allocation needs to be $243,000 (50% of the total), but we only have $225,000 in the non-registered account. So we’ll have to sell some bonds in one of the registered accounts and use it to buy equities. International equities are the least tax-efficient (because they are not eligible for the dividend tax credit and they have a higher yield than US equities), so they should be the first candidate. Here’s one solution:

In many ways it would be simpler to just use a 50-50 asset mix in each individual account: that would certainly make rebalancing easier. But it also mean a lot more transaction costs and probably a higher tax bill, especially if Anne used bond ETFs in the taxable account. Using the above strategy takes a little more planning and experience, but it should produce the best results.

I have taken this approach with the finances of my wife and I. We treat all our investment accounts as one big portfolio in terms of asset allocation goes. Unfortunately, we have a few more accounts than ideal because of various work related investments where you are mandated to invest with a specific company to get the matching bonus. I have consolidated those in the past but new ones keep cropping up :)

I’m also not very good at rebalancing and I just try to do what I can with it when there is new money or dividends/interest to invest.

Two questions:

1- Over the long term, we expect stocks to have higher returns than bonds. Won’t that have tax consequences, later, as Anne’s taxable account should grow faster than Henry’s accounts?

2- Given the possibility that Anne and Henry divorce, one day, could the suggested division of investments have undesirable yet significant consequences in case of a split up?

ccpfan – my dumb guy interpretation:

1 – The fact that dividends and capital gains, especially for canadian companies, are taxed at a lower rate trumps this, I think.

2 – In the event of split up, investments are generally all looked at as joint property and split, unless there is a prior agreement that states otherwise.

@CCP fan: The answer to your first question is not straightforward, but Justin and I considered it at length in a recent white paper. Our conclusion was that it if you need to hold some of your assets in non-registered accounts the order of preference is Canadian equities, US equities, and then international equities:

https://canadiancouchpotato.com/2014/04/24/do-bonds-still-belong-in-an-rrsp/

As Craig anticipated, if a couple splits up assets are generally divided equally unless there is a marriage contract specifying otherwise, so this is not usually an issue in portfolio construction.

Just wondering why all the non-registered funds are held with Anne?

Is it just to reduce the number of accounts?

Or is it possibly because Anne has a lower taxable income and it is more tax efficient to hold investments with her?

Hello, there is obviously merit in allocating bonds to non taxable accounts and equities to taxable accounts from a yield perspective. However this does not reflect the fact that equities are usually much more volatile than bonds and one usually will face more important tax disadvantages at the time of rebalancing if he needs to sell equities and take a large capital gain tax hit (such as in this market cycle where equities are at record highs and yields on bonds are historically low). I think the common approach is flawed in disregarding those capital gain consequences in allocating among various account types and focusing solely on yield taxation, especially with a large portfolio. I would like to see an analysis that considers this issue.

@Scotty: In the example, Anne has little RRSP room so she needs to hold most of her savings in a non-regsitered account. Henry does not have this problem. Regardless of their individual marginal tax rates we can’t put Anne’s non-registered savings in Henry’s name.

@Phil: As we explain in the white paper linked above, there is no perfect solution and the optimal one can only be known in retrospect. We believe it makes sense to focus on what we know: the tax on distributions is known in advance and the bill arrives every year. Capital gains/losses are unknowable in advance and the investor has some control over when to realize them.

Moreover, the problem is not fixed by holding equities in the registered accounts. If stocks were to fall in value the investor would be required to sell fixed income, which would also realize capital gains. And indeed, with equities in the non-registered account there is actually more opportunity to take advantage of tax-loss harvesting opportunities to further defer any taxable gains.

In this example we’ve also assumed that both spouses are adding new money to the accounts, so a lot of rebalancing can be done with cash inflows, which further reduces the need for selling equities and facing large capital gains.

@CCP, Phil, ccpfan: Completely agree with all the discussion around this and all the merits cited in the linked whitepaper. As always this is a personal decision that varies with accounts, sizes, allocations, etc.. However for a younger person today, and although I completely agree that returns are not knowable in advance, I do feel there is merit in the idea that you might want to seriously consider filling TFSAs with equities rather than bonds (even if this means holding some bonds in an unregistered account). All the reasons CCP cites are completely valid, however I respectfully suggest that, for a young person, it might be worth looking seriously at this. The long term expected out performance of equities (which you implicitly must believe in to implement passive investing), coupled with not-so-insignificant probability that taxes may be higher in the future, to me suggest that trying to “grow your TFSA” is probably a pretty valid approach to take.

@Willy: I should point out that the white paper specifically excluded TFSAs from the discussion and focused only on RRSPs. There is nothing wrong with your reasoning, but for practical purposes TFSAs represent a fairly trivial amount of money at this point ($31,500 if maxed out). The asset location really only becomes important with larger portfolios where all registered room is maxed out and there are significant savings in taxable accounts. Very few young investors have this problem.

Remember, too, that asset location decisions are not permanent. Indeed, many wealthy investors will find that their non-registered accounts become a greater and greater proportion of the portfolio as they get older. What we often see is investors holding equities in their registered accounts for years and then gradually moving those equities into non-registered accounts as necessary. (Note that when I say “moving” what I really mean is the equities in the registered accounts are sold and bonds are purchased with the proceeds. Then an equal amount of equities is purchased in the non-registered account to keep the overall asset allocation the same.)

I have an indirectly related question about the logistics of the one portfolio option (not the philosophy behind it). My wife and I are assembling our couch potato strategy and likely will have six accounts in total. (two tfsa, two rrsp, and two non-reg). Is it worth while to open an joint account for the non-reg portion of our portfolio? I realize that it will be easier to save on tax, but does that not also open up the other spouse to significant liabilities (i.e. lawsuits, bankruptcy, etc)?

Thanks.

@CCP: Agree for sure. Certainly about the relative size of a TFSA today, for someone with even a modest portfolio, and a shorter time horizon, it’s not a big deal. This is why I actually specifically referenced younger investors. If treated correctly, $31k today for a young person, and contributed to yearly, could easily become hundreds of thousands for that person in retirement. Such that the phenomenon you mentioned of non-registered accounts growing as investors age/accumulate may not be the same for the current younger generation. All the more reason why I think you want to take a long view, and grow that account. Until the government changes the rules, that is!

Assuming there is room, I would argue it makes sense to keep the equivalent of one to two standard deviation in equities in non taxable account to be able to do annual rebalancing tax free. The bulk is yielding low tax in taxable account and the capital gain issue is significantly minimized through the non taxable component. If there is some thinking done around that, I would love to know about it.

Agree this issue is somewhat reduced when new funds are added annually.

@Rich: In most cases, couples should ensure that their non-registered accounts are jointly held. Usually that means the spouses are “joint tenants

with rights of survivorship.” That way if one spouse dies the other immediately becomes the sole owner of the account with no need for probate. However (and this is very important!) that does not provide an opportunity for income splitting. In our example above, Henry can be a joint account holder with Anne, but if Anne is making all of the contributions to the account she is on the hook for the taxes on any income. If the spouses are splitting the taxes 50-50 they must be able to prove they are both contributing to the joint account if they are challenged by CRA.

This document is quite helpful:

http://www.assante.com/advisors/fmalinka/documents/TEP-EP-Joint%20Accounts.pdf

I have 7 different accounts at the moment do to company programs and the likes. After reading one of Dan’s posts from a year or so ago I decided to balance the accounts as three seperate groups:

1) My LIRAs

2) My RRSP & DC that are in the company accounts

3) MyTFSAs and RRSPs that are in my personal accounts

It has been working out quite well for me.

For purposes of balancing or rebalancing, should you take into account the fact that monies in registered accounts are subject to tax on withdrawal, and therefore are not equivalent to monies held in a nonregistered account? Would it be wise therefore, when balancing, to notionally reduce the value of the RRSP investments by e.g. 30% to take into consideration the tax consequences? Thank you.

@ CCP:

“In most cases, couples should ensure that their non-registered accounts are jointly held. Usually that means the spouses are “joint tenants

with rights of survivorship.” That way if one spouse dies the other immediately becomes the sole owner of the account with no need for probate.”

It should be noted that these comments do NOT apply to Quebec residents. There is no “joint tenants with rights of survivorship” status in that province – joint accounts are held as “tenants-in-common”. Furthermore, wills drawn up by notary in Quebec are exempt from probate, facilitating access to joint accounts by the surviving spouse in that case (as a general rule Quebec residents should consider having their wills drawn up by notary, as these have other advantages aside from probate exemption).

@Stephen: That’s a great question I have been asked before. Certainly one needs to be aware that there is a tax liability in RRSPs that does not exist in a non-registered account. However, I don’t see how one can consider that when managing an asset allocation. For example, suppose you held $200,000 in bonds in an RRSP and $200,000 in stocks in a non-registered accounts. Can you really say your allocation is not 50-50? If so, what is it? How would you rebalance if stocks rose and bonds fell in value?

William Bernstein addresses this question in his recent book, Rational Expectations. It’s a US context, but the principal is the same: “Some maintain that in calculating allocations you should adjust downward the assets in your taxable accounts and [tax-sheltered] accounts by their estimated future tax exposures… I largely disagree. To the extent that the assets are fungible among your accounts, it doesn’t matter where your assets are. Since there’s nothing that prevents you from selling a given dollar amount of equity in your sheltered account and buying it your taxable account, why should the exact stock/bond allocation of each pool matter?”

@Steve: Thanks for making this point. The truth is that a very large share of personal finance advice for the rest of Canada does not apply in Quebec!

Sometime ago I downloaded and implemented the two spreadsheets that you kindly provided in previous postings, one for rebalancing individual accounts and the second one for rebalancing over multiple accounts. I re-jiggered them, combined them, and generally Franknsteined them to meet my own needs. (I was taking an Excel course at the time, so it gave me a project to work on to learn the course fundamentals). The individual accounts can now be rebalanced individually and by setting target allocations on an individual level, it then updates the target allocations and allows rebalancing on a multiple account level. I really went over-board on the exercise and tied in an updateable net worth statement, an annual cash flow tracking sheet, a rental property income sheet, a detailed listing of each ETF including their yield, purchase amount, and MER fees, and finally a sheet that allows targeted withdrawal amounts allowing for input of inflation adjusted income and monthly/annual yield amounts.

The good news is that by simply inputting changing yield amounts, inflation rates, rental income, and rebalancing amounts in each account, I’m able to see both the big and little picture in one workbook.

Thanks again for providing the rebalance spreadsheets that sent me happily down the rabbit hole. Oh, and the new workbook I built, (with your help), helped get me a 97% for the final grade in the Excel course. Thanks!

“Regardless of their individual marginal tax rates we can’t put Anne’s non-registered savings in Henry’s name.”

I’m curious about this statement. Consider this example:

A married couple Jon and Jane.

Jon making 90k and Jane making 10k.

Assume RRSP and TFSA do not exist.

500k of investable cash.

Can the 500k (and all future savings) not be held in Jane’s name so that all investment income is taxed at her lower marginal rate?

@Scotty: It depends where the $500K came from. If it was an inheritance from Jane’s family then, yes, it can be held in her name and taxed in her hands. But Jon can’t simply save a large portion of his income and say it is Jane’s money. If he does, the income and any gains on that money will be taxed in Jon’s hands:

http://www.taxtips.ca/personaltax/attributionrules.htm

That said, it is possible for Jon to lend Jane a sum of money and charge the CRA’s prescribed rate of interest (currently 1%). The money could then be held in Jane’s name and taxed in her hands.

Interesting…I wonder how the CRA knows where the money came from. So for me personally, my wife and I have a joint chequing account and all pay cheques are deposited there. The pay discrepancy isn’t nearly as extreme as my example, but I still make more money. Maybe the best way to go is just a joint non-registered account + TFSA x 2 and RRSP x 2 for a total of 5 accounts.

@ Scotty:

Keep in mind that you are allowed to contribute to your spouse’s TFSA, and that money would thereafter be considered to belong to your spouse. No tax implications of course – but when a higher income spouse contributes to the lower income spouse’s TFSA, that provides for a bit of “levelling” in the respective investing/ savings amounts by each of them.

@Scotty: A lot of couples in your situation will just split the taxes 50-50 on the non-registered account. The CRA is unlikely to question that. Many couples just structure things so the higher income spouse pays more of the expenses which frees up more of the other spouse’s income for investment.

@CCP: Thanks for a great article. I have to confess that I am guilty of setting up multiple accounts with the same 60/40 asset mix. I find that it is just easier for me to look at it that way. Rebalancing costs are kept to a minimum by using a discount brokerage and your recommended index funds when ETFs are not cost effective.

The difficulty that I have always had with the common shared approach is that while it is tax efficient, there are never really any numbers mentioned were one can compare the costs of one approach versus another. Also, every family’s situation is unique, so a common set of assumptions may not be very helpful.

You once asked me a long time ago, about what I would be looking in an adviser service versus a DIY approach. I can say now that this is something that I have no trouble leaving in the hands of an advisor and it is one of the things that would differentiate PWL from the run of the mill advisors (Salespeople) and the DIY crowd.

So, tax efficient structuring of multiple accounts, along with setting up and monitoring of a monthly living stream combined with monitoring the accounts so that they grow with inflation and are self sustaining are the items that I will be looking for from an advisory service.

cheers,

rob…

FYI, the comments above that investments are split 50-50 on break-up need to be qualified as 50-50 property division applies to married couples only in many provinces (including Ontario), not to common-law couples. For common-law, I presume a contract specifying 50-50 division would be beneficial.

This is a great article and it’s definitely something that married couples should consider.

Forgive me if this was already explained – or if I’m missing something..but could you explain how the equities in the non-registered account result in a lower tax bill?

“…With this setup, all of the bonds are in tax-sheltered accounts and the equities are in Anne’s non-registered account, which is likely to result in a lower tax bill.”

@SimpleRyan: Asset location is a big topic, which I’ve written about here, among other places:

https://canadiancouchpotato.com/2014/04/24/do-bonds-still-belong-in-an-rrsp/

@Robert_M: In our white paper on asset location we estimated the benefit to be about 30 basis points annually. A Vanguard study using a different methodology arrived at a similar conclusion. If an advisor charges 1% and that fee is deductible in non-registered accounts, and then you can add 30 bps with effective asset location, plus the disciplined rebalancing, tax-loss selling and planning services it’s pretty easy to make a value proposition.

Hi Dan,

Another aspect other than taxes to consider when making asset location is the management expense ratios. Take for example two spouses with different employers each offer RRSPs and define contributions having a different investment manager selection to choose. Some employers may have a good bargaining power than others and are able to negotiate better fees — even for active managers. For example, my employer offers an excellent small cap active fund for less than 75 bps which cannot be found at the retail level. So when doing an optimization exercise, take my situation, the family small cap allocation is entirely in my DC employer plan and adjusted my wife’s RRSPS accordingly with cheaper large cap indexed funds in her offerings. It may seem to complicate things but is worth doing the analysis, at least the first time or when an employer offers a new investment choice.

Re Stephen’s question about the tax effects and your reply CCP, quoting Bernstein. I think Mr Bernstein has it wrong. What matters is not whether you can buy and sell across accounts, replacing assets. It’s rather what you actually own (the government owns the other part) and can spend after tax. I wrote about how I would (and I do so for myself) handle this here – http://howtoinvestonline.blogspot.co.uk/2012/11/tax-adjusted-asset-allocation.html

@CanadianInvestor: That’s an interesting point, thanks for that. You’re probably right… using pre-tax allocations for computing asset allocation does distort the post-tax picture of the volatility of your portfolio.

@CCP: You said something about the fact that “a very large share of personal finance advice for the rest of Canada does not apply in Quebec” which is definitely not true. Tax advice might differ between provinces (not limited to Quebec) but investment principles should not really change.

And regarding this article, divorce statistics should also be considered. We all say that it won’t happen to us but approximately 40% of marriages end in divorces. This article makes the assumption that assets were generated during the marriage and they will be split 50-50 but what if it’s not the case ?

@ Linda Rocco:

“You said something about the fact that “a very large share of personal finance advice for the rest of Canada does not apply in Quebec” which is definitely not true. Tax advice might differ between provinces (not limited to Quebec) but investment principles should not really change.”

CCP spoke of “personal finance advice” not just investments, and he was absolutely correct.

One issue is that Quebec is a Civil Law jurisdiction, and so such matters as successions and property law – which are obviously directly related to personal finance – differ substantially in many cases from the principles found in the other (Common Law jurisdiction) provinces. For example, in my previous post (to which CCP was replying) I pointed out the lack of JTRS joint accounts in Quebec, unlike all the other provinces, and the distinct benefits of notarial wills there.

There are other issues as well, such as the distinct regulatory regime in Quebec, and the fact the Quebec tax system is autonomous from the federal system (Quebecers file an entirely separate and vastly longer second tax return directly to Revenu Quebec, which has a number of unique wrinkles). These might obviously have an effect on investment principles if the taxation of investment income differed from the Canadian norm.

Is there an opposite of a wash-sale? Selling for a capital gain and buying a similar ETF (e.g. selling XIC and buying VCN) within the same account and owing no tax. I’m combining family investments and the tracking spreadsheet is getting out of control.

Dan, do you think Scotiabank Index Funds are any good or should I just transfer my RRSP to Scotia’s iShares? I have a fair chunk in Scotia’s Innova Balanced Fund.

Scotia’s Index Funds seem to have pretty low MERs but am I missing too many other hidden costs? Are administration fees included in MERS usually?

I did enjoy your Moneysense book and hope to get a few things changed around. Still reading lots here first though.

Thanks for your time.

@Ron B: Scotia’s index funds cost over 1% on average. If you’re willing to pay that much, I think the Tangerine Investment Funds offer more convenience. If Scotia charges any administrative account fees (such as an annual account fee on the RRSP) it will not be included in the MER.

@Don: If you’re selling an ETF to harvest a gain (as opposed to a loss) there is no need to buy a different ETF. There is no such thing as a “superficial gain rule.”

https://canadiancouchpotato.com/2013/10/21/tax-loss-selling-with-canadian-etfs/

As per Scotty’s question above regarding taxes when one spouse makes more than another, do you know how that works if all money made goes into a professional corporation? Through the corp the salary/dividends can be whatever you decide it to be so would there be any problems with investing through that even though one spouse makes considerably more than the other (before the money ends up in the corp)?

Thanks

Dan, after reading a bit more maybe I’d best do the comm-free ETF mix at Scotia iTrade for my 90K and then a TFSA at TD with the TD e-series.

Wish I could find a decent mix of index funds at Scotiabank to keep everything in one place though. Maybe it’s best to not keep all my eggs in one basket though.

Instead of managing a multiple family account I’ll need to manage multiple accounts… same things apply I’m sure. I imagine if I need to it may even involve having my bonds in one place, my stocks in another, etc as long as I’m following the percent risks I’ve set up for myself.

Things are getting a bit more complicated. :-)

Thanks again.

Do you know anything about insurance company products. A family member is starting to move to a DIY investment strategy with index funds. An advisor with an insurance company wants them to invest in a product that Empire Life offers that has a 5% simple interest, not compound interest, guaranteed for 3 years. They are trying to decide if this is a good product for their fixed income part of their portfolio. The advisor has told them he makes 1.5% from Empire Life and that there are no other fees.

@Jon: Let me start by saying if you have a professional corporation you really need to get professional tax advice. In general, any money retained in the corp is taxed at corporate rates. Money can be removed from the company via salary or dividends, at which point it is taxed in the recipient’s hands. All shareholders need to receive the same amount of dividends per share, but you can vary the salary, which may offer some opportunity for income splitting. But you must pay employees a salary CRA deems to be reasonable.

@Ron B: Whatever you decide, I would encourage you to use a single brokerage. I’m not sure what circumstances would ever make it a better choice to spread it across two. If you use Scotia iTrade for the RRSP why not also use it for the TFSA?

@Darby: It sounds like your family member is being offered one of the many “guaranteed minimum withdrawal benefit” products. I can’t say too much without knowing which product it is, but suffice it to say that these products are complex and designed to get the investor to focus on the income (5% interest!) and ignore the very high costs and the complex conditions. There are always simpler and cheaper options.

Sorry to take up space here with my newbie questions but if I went with Scotia’s iTrade for both RRSP and TFSA I could/would set up both funds to have the same components? Or would it be smarter to diversify there too?

I thought one might be better to be in index funds and the other in ETFs.

And if I used commission free ETFs for both then I could still do monthly contributions to the TFSA and adjust it as needed? The RRSP I’d adjust at least once a year (or less if not needed).

I thought I could do this but maybe ‘hands off’ with Scotia’s Tangerine would be better for me.

I’d better go back to the archives and your Moneysense book.

Thank you.

The math shows that with rebalancing, the Asset Location decision becomes much less important. See the spreadsheet model allowing variable inputs. Rarely does the outcome vary by more than 5%-10% after 30 years. (the YearByYear tab of http://www.retailinvestor.org/Challenge.xls ) That is just not worth the trouble. There are too many other unknowns that will end up having a much larger effect.

I think the trade off is personal – between a) holding all of each asset in only one account vs b) the simplicity of rebalancing when each account is considered separately.

Certainly don’t agree with the referenced articles arguing for holding debt in tax-sheltered accounts. High growth assets are best in tax-sheltered accounts unless their effective tax rate is really, really low. See http://www.retailinvestor.org/rrsp.html#taxfree

@Retail Investor: Thanks for sharing this site and analysis re the potential benefits of holding high growth assets in RRSP instead of debt, contrary to traditional advice. It would be helpful if CCP could look into that article and let us know his thoughts and whether that influences the analysis in this post (or not).

@Phil: Justin Bender and I spent several weeks examining this question when preparing our white paper on the subject:

https://canadiancouchpotato.com/2014/04/24/do-bonds-still-belong-in-an-rrsp/

Unlike any previous article we’re aware of, we used actual data rather than hypothetical assumptions about the returns of stocks and bonds. (Albeit for one 10-year period.) As we made clear in the paper, the right decision can only be known in hindsight. But when you manage other people’s money (and Justin manages $120 million for about 100 families) you need to make a decision based on your best analysis.

Our paper showed that the total after-tax return was higher with the bonds in the RRSP during the period we looked at. Moreover, we articulated several reasons why expect that to be the case going forward.

The recent historical returns from Treasuries has been GREAT. All because interest rates were steadily falling. Since Asset Locating assets with BOTH high returns and high effective interest rates is the very, very best, the historical allocation of bond to tax-sheltered accounts would have had the best outcome (along with REITS which had the same high tax rate and high return). All that corresponds to the analysis of the website linked above.

But we are now making decisions about the future where interest rates cannot fall another 10% because they are already down at 2%. Historical returns are irrelevant. Hypothetical assumptions (i.e. forward looking estimates) are exactly what you need.

@CCP: Your paper doesn’t really “articulate[] several reasons why expect that to be the case going forward”… it just presents a list of advantages and disadvantages of both approaches at the end. (The paper does speculate that future capital gains from equity ETFs are likely to be lower, but that seems largely inconsequential in my view.)

I think this is the one point on your website where you’re simply wrong from a mathematical standpoint. There is an upper bound to future bond returns, unless furture nominal interest rates go negative. Add that upper bound to your model and it becomes virtually impossible to conclude that bonds should go in an RRSP. Note that this is not a prediction about what bond returns will be in the future, just a mathematical consequence of the assumption that nominal bond returns cannot go negative.

Interesting discussion on a complex issue. I have a couple thoughts on this.

1) Agree wholeheartedly with those that state that it is impossible to know returns in advance. While I understand how a bond works and get the mathematics, I am always loathe to believe even seemingly “certain” statements. That being said, we have to fundamentally accept that equity returns are going to be higher than bond returns. If they’re not, then, well, really, everything on this site and 98% of modern financial theory has to be thrown out with it. So equities must outperform bonds – by how much is not certain or knowable.

2) One thing I think has been missed in CPP’s paper is that investors usually have at least SOME control over RRSP withdrawal timing. It states that timing of cap-gain realization can be controled, yet I would hazard that for the vast majority, it is probable to think that timing could be arranged such that RRSP withdrawals happen at a much lower tax rate than the deposits. If this can be arranged, then I think it becomes clear from Retail Investor’s charts and other simple math that heavy favor should go to placing assets with higher returns in RRSPs, especially when talking about long horizons. Per the above, you have to accept that this is equities.

3) The one big element here that I think people are missing is that there is one, big, important actor that can change all of this in a heartbeat, and that’s the government. Everyone here knows the state of federal and provincial finances and I think would all agree that there’s every chance that in the future, governments will change taxation rules. So, which will the Canadian Federal government choose 20 years from now:

-Choose to tax capital gains the same as income (ie doing away with the 50% rule) and/or do away with the eligible dividend credit, or

-Choose to raise personal income tax rates

I think neither of those is far-fetched, and both would DRASTICALLY alter the outcome of this discussion, yet in completely opposite directions.

So I think that for all this pontificating and calculating, someone in Ottawa, 20yrs from now, will likely make a decision that will change the parameters so much that all of this is rendered moot anyway

Hi everyone – I thought I’d add a few more comments to the discussion:

1. Although yields on bond ETFs are extremely low right now, average coupons are higher. The weighted average coupon on the iShares Canadian Universe Bond Index ETF (XBB) is 3.77% (3.44% after-fees). This is currently higher than the interest equivalent dividend yields on Canadian, U.S., or International equities (so you will likely be paying more annual taxes each year by holding bond ETFs in your taxable accounts).

2. There are fixed income products available that have lower coupons than premium bond ETFs (such as GICs or the new BMO Discount Bond Index ETF (ZDB)). An argument can certainly be made for holding these types of products in taxable accounts.

3. Our analysis assumed no new contributions into the portfolio. New contributions would have lowered the amount of realized capital gains from rebalancing over the period studied (further improving the results for holding equities in taxable accounts). If an investor was no longer contributing to their portfolio and only withdrawing, they should consider holding more low-coupon fixed income securities in their taxable account.

4. Our analysis assumed no tax loss selling strategy was implemented. This would have also allowed for a further deferral of capital gains taxes from rebalancing.

5. When there is another downturn in the equity markets, TFSAs and RRSPs holding fixed income can easily be switched to equities in order to rebalance the portfolio. As equities recover, they can be switched back to fixed income securities with no tax consequences.