If your portfolio includes a broad-based bond index fund, you’ve probably noticed its value has fallen significantly over the past several weeks. Judging from recent e-mails I’ve received, the reasons for this decline are not always clear, so let’s take a closer look.

Most investors understand that when interest rates rise, bond prices fall. But there are many different interest rates, and they all affect your bond fund in different ways. The shortest of short-term rates is the target for the overnight rate, which is set by the Bank of Canada to control monetary policy—in other words, to keep inflation low. This rate influences the prime rate banks use to price variable-rate mortgages and lines of credit, so it’s the one most widely discussed in the media.

The Bank of Canada has kept the target rate at 1% since September 2010: that’s more than 32 months, the longest period it has ever remained unchanged. Meanwhile, the prime rate has held firm at 3% during this same period. I’ve been asked by some investors why they’ve seen their bond holdings fall when “interest rates haven’t gone up.”

But as I’ve mentioned, this short-term benchmark is only one of many interest rates. The yields on two-year, five-year, 10-year and longer-term bonds move independently of the target rate, and these are the rates that affect your bond index fund. They’re rarely reported in the financial media, but you can follow them on the Bank of Canada’s website.

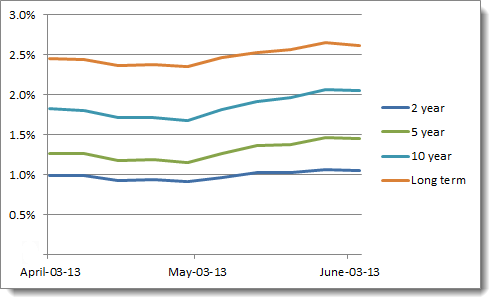

The chart below shows the yield on several benchmark Government of Canada bonds over the last two months:

Notice that all of these rates moved upward in May, and the steepest line belongs to 10-year bonds, which have seen yields jump from 1.68% at the beginning of the month to 2.07% on May 29. As a result the iShares DEX Universe Bond (XBB), the BMO Aggregate Bond (ZAG) and the Vanguard Canadian Aggregate Bond (VAB), all which have an average term of about 10 years, saw their market prices fall significantly during the month:

The price is only half the story

There’s another extremely important point to understand. Whenever you look up bond ETFs using a tool like Google Finance, as I did above, the results are highly misleading. These charts show only the change in market price, not the interest payments paid to investors in cash, so they do not reflect the total return of your bond ETF.

These days, with virtually all bonds trading at a premium, you should expect the market price of your fund to fall even if interest rates hold steady. However, the cash payments from the underlying bonds are in the neighbourhood of 3% to 3.5% for broad-based index funds, which will offset at least some of that price decline. Indeed, the three ETFs above each delivered a total return of more than 1.5% during the 12 months ending in May, even though their market prices fell considerably during that time.

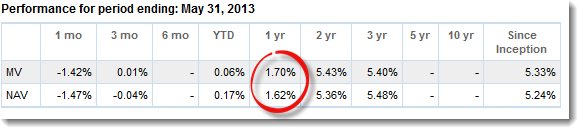

Remember this when you look at your brokerage statement. Say you bought ZAG on May 31, 2012, and paid $15.96 per unit. Exactly one year later its price was $15.70, so your statement would show a loss of –1.63%. However, the fund’s total return over that period was +1.62%, because the interest payments more than offset the price drop. You didn’t lose money, even though I’m sure some investors thought they did.

An individual fund’s total annual return never appears on your statements, so you should periodically visit your bond fund’s website to see how it’s really doing. Click the “Performance” tab to see the total return on the fund including price changes and reinvested interest payments. Here’s what they look like for ZAG:

If yields continue to rise, bond funds can and will deliver negative returns even after accounting for interest payments, so you should be prepared for that. Remember why bonds are in your portfolio: they lower overall volatility and provide a cushion when equities inevitably suffer a downturn. If bonds do have a difficult year, that’s not a reason to abandon them: it’s an opportunity to rebalance.

What would happen to bonds for example if interest rates climb say by 3% over the next 2 or 3 years – which really now may not be out of the realm of posibilty? People who have Bond funds with high mer’s may also have to consider that fee alone may negate any gain or even cause a loss, for the next while as well. (People with work pension plans that have little choice in selection could be affected more with their high fee fund offerings).

Maybe slowly laddering into GIC’s now as interest rates rise within an RRSP with a portion of your money might be something to consider?

@Paul N: There’s no question that fees are much more important in this era of low rates. There are funds with a yield to maturity of 2% that charge more than 1% in fees, which is outrageous.

Regarding the effect on rising rates on bond funds, see this post, where I asked iShares to run some simulations assuming a 1% hike across the yield curve for three years in a row. There would certainly be some negative returns, but my guess this is not nearly as bad as many people expect:

https://canadiancouchpotato.com/2012/07/03/how-will-rising-rates-affect-bonds/

There’s nothing wrong with a GIC ladder (or short-term bonds) if that’s in line with your goals. But be wary of using phrases like “now as interest rates rise.” Interest rates rose (past tense) in May. There is no reason to assume they will continue to rise this month or next. We saw a similar hike in 2012, and it was immediately followed by another rate drop. If we have a correction in the equity markets, rates will almost certainly fall. That’s why it’s important to have a long-term target and stick with it. Otherwise you become a market timer.

Thank you so much for this explantation. I did indeed buy bond ETF’s a year ago and should rebalance now. I am glad that you reminded us how weird it will feel to put money into what feels like a losing proposition, but that is just so that next year or the year after, we feel great about the overall mix.

It looks like there have been particularly big moves in the yields Friday and today. I would welcome higher bond yields since they will provide much better long-term returns regardless of the short-term impact.

Thank you for that fast reply. My work pension plan has a 1.6% mer on the bond offerings. I have no other bond option. I feel if I will be faced with GWL skimming off that amount for the next few years (coupled with most likely a low return). I don’t have much of a choice. I’m sure I am not the only person in a company pension plan out there that is in this boat.

I won’t get 100% out of bonds. By transferring a portion of what I have into the GIC offering in our plan I feel the risk is minimal. If the Bonds suddenly go up I still have bonds. If they go down further I will have buffered the drop with a few GIC’s to offset some of the loss. ( And I’ll feel better I saved some of my 1.6% fee :) )

@Paul N: At 1.6%, the fund manager is getting three-quarters of the yield to maturity. It’s absurd. Is there a way you can structure your overall situation so you your work plan is 100% equities and the fixed income component is held in a self-directed RRSP where you can take advantage of lower-cost bond options?

Let me see if I have this right… so as interest rates on long-term bonds rise, the demand for the older bonds in the fund (which have today’s lower coupon) will decline, so the demand and thus price for the existing bonds being held will go down. But as these older bonds in the fund reach maturity and are replaced with higher-coupon bonds being issued under the new, higher rates, the fund itself will gradually fill up with new, higher-coupon bonds – so this means that if you’re holding it long enough to get to the point where interest rates start falling again say in ten to fifteen years (none of us know when), then you’ll be holding a fund full of comparatively high-coupon bonds which will be in demand relative to the current offering. Is that right?

I have the same problem as Paul N. I’m glad to hear you are offering suggestions, but my company has a DCP and offers the choice of about 20 mutual funds and that’s it; all of which are loosing money, even though I have balanced to them within 1% of the Couch Potato Portfolio (so how have they catastrophically missed the S&P 500 rise I dunno – but that mutual fund is down 10%!!). Many of the employees are crying out to be able to use self-directed RSP’s, which we are welcome to use, but if we do, the Company won’t contribute to them. But we know we are being screwed by fees and poor returns of the mutual fund company!

I am underwhelmed by the fees on this account, but at the end of the day, all I can do is grit my teeth and say my Company is matching my contribution so I am ‘making’ more than the mutual funds are loosing. How long that will continue, I don’t know. But it is a weak supportive thought as I have watched my entire portfolio loose about 20% over the last year…

Also, since the company will only match a certain percentage of my contributions, I am only contributing the maximum amount that the Company will match. The rest I am putting into a self-directed RSP, which is slowly being bought into alignment and balance with the couch potato portfolio (because being a ‘new’ Canadian, I didn’t start out with a Couch Potato Portfolio and do not have a lot of room to contribute each year…)

How do you think this fits in with floating rate bond ETFs that offer decent yields and much lower duration risk? I’m thinking of XFR as a lower-risk option, and HFR as a higher risk.

@Alex: You pretty much nailed it.

@Cybamuse: It’s hard to imagine how any portfolio could have fallen 20% over last 12 year. If your only choice is high-cost, terribly managed funds, is there a way to do the opposite of what I suggested to Paul—that is, get the maximum company match by using the most conservative fund you can get (maybe a money market fund) and then keep all your equities in self-directed RRSPs and TFSAs? And maybe transfer out as much as you’re allowed each year?

@Andrew F: I wrote about floating rate notes here. As always, there’s a tradeoff you need to consider:

https://canadiancouchpotato.com/2013/05/02/understanding-floating-rate-notes/

Wow as a DIY guy I really never thought of it that way. Just the opposite. I always think of my fallback as my work pension so I kept the “safety” portion in bonds there. I invest in securities outside of it in my TFSA and SD-RRSP. Your idea of course makes sense. Just some of those DC equity funds (you know the ones that they claim are low to medium risk on their website?) took such wild swings of volatility down 55 to 60% in 2008 – 2009 but never really came back up the same way they went down.

I have been trying to pressure our people in power at work to do a full review and comparison of our DCP to other companies offering group plans. At least threaten our existing provider that we will leave if they don’t offer other low cost options or a few index funds as option 2. It’s finally met “some” success but unfortunately when the CEO and our accountant do not know the difference between a GIC and a bond and invests 100% only in GIC’s…claiming that’s the only safe thing to do, its a little tough to explain. A discussion about inflation and it’s effects on GIC returns was also lost on them. An on-line MER calculator (wheredoesallmymoneygo.com) was actually one tool I used and it helped make my point – people so resist change. I have worked in one place for quite some time – I have to put it out of my mind regularly of how much I lose (bleed) in fee’s every year.

@Paul N: It’s so disappointing to hear stories like this. One of the benefits of a workplace plan is they usually qualify for much lower pricing than retail funds, if for no other reason than there is no advisor to pay. It’s a shame that’s not the case here. And there’s really no excuse for not offering at least some kind of indexed option. My suggestion assumed that you had some reasonable equity options in the DC plan, but it sounds like that may not be the case either.

Thanks for your support and comments, love your Blog!

I am in the same boat as Cybamuse & Paul N. My employer DC pension plan matches up to 5% of the employee contributions. It is run by one of the biggest players in the Canadian DCPP business. Overall it is a decent plan and very generous on the part of my employer. However, the bad part is that the investment choices consist of about 25 or so mutual funds. The mutual fund MER’s are lower compared to retail, but compared to ETF’s the MER’s are absolutely outrageous.

My only option to get my investments out is to leave the plan and forfeit the 5% matching. Not a great option. In addition, I strongly suspect that behind the scenes, the DCPP carrier is indexing themselves and repacking in a “mutual fund” wrapper which gets marked up with higher MER’s and then sold to the employees.

In my opinion a lot of money in MER’s is being made on the backs of the employees, not only at my company but at all other employers across Canada.

How can we put pressure on these large work DCPP plans to reduce their fees?

Paul, would you be able to put together a comparison that shows how the funds have underperformed their benchmarks? It sounds like you could pretty easily make the case that they are all terrible and there are similar options with much better performance (ideally, from a low-fee provider). If these funds have all been around for a while and you focus on the long-term record, the difference should be pretty clear. Ask the CEO what would happen if the business delivered 60% of the value that competitors do at twice the cost…

My employer is using manulife and we can select our index funds. My MERS are all competitive to TD-series funds. And performance has been well above expectations. I decided to take the option of maxing out my RRSP’s aswell as the pension plan through pay deductions. So fight hard, there are great providers out there. And I hope you’ll end up getting a pension plan that’s a great match.

That was TD e-series funds, which I also hold in my TFSA

I have a questions reagarding this

“If yields continue to rise, bond funds can and will deliver negative returns even after accounting for interest payments, so you should be prepared for that”

I was under the impression that you will get the yield to mataurity of fund if you hold it for the duration regardless of what happens to interest rates?

For example, VAB has a current YTM of 2.1% and duration of 7.2 years, is it possible to lose money if you held it for 7 years?

thanks

@karim: Yield to maturity and duration are not precise, but they are good estimates. You’re correct that you will not lose money if you hold a bond fund for a period equal to its duration. I was only referring to negative returns over shorter periods. It’s certainly possible for a fund like VAB to lose money over three years or so if rates move up steadily. There was a period in the 1960s when bonds suffered negative returns for a few years running. But these losses were small, and new higher-coupon bonds eventually led to a relatively speedy recovery.

Of course, you could try to time the market by selling bonds when you think rates are about to rise, and then buying them back when yields are higher. Ask the gurus how that’s worked out over the last four years. :)

http://www.forbes.com/sites/petercohan/2012/02/25/bill-grosss-bad-call-cost-investors-5-7-trillion/

http://blogs.marketwatch.com/thetell/2013/05/31/pimcos-total-return-fund-headed-for-worst-loss-since-2008/

If you think nominal bond ETFs are having a rough time, take a look at real-return bond ETFs. I assume their poor recent performance is due to their long duration (>15 years). Does anyone know if there are any real-return bond funds with a shorter duration (say less than 10 years)? I’d like an instrument that is less influenced by interest rates and more influenced by inflation.

@Smithson: Yes, RRBs are affected by both interest rate movements and expected inflation. And because of their long maturities and low coupons they have a long duration and they can be quite volatile in the short run.

https://canadiancouchpotato.com/2013/02/28/ask-the-spud-the-role-of-real-return-bonds/

Unfortunately, there are very few Canadian RRBs (there are only six federal government issues) and they all have long maturities. In the US, it’s very different: the federal government issues new TIPS (Treasury Inflation Protected Securities) every year. Not sure why the situation is so different here.

@Dave – I agree with you! I am loosing about 10% in fees each month with the company plan, and most of the mutual funds I am forced to choose from are broadly following indexes. No wonder I am loosing money…

@Dan I like your advice to restructure to put everything into the most conservative funds my company has – although I don’t like the fact they are the ones loosing the most right now. But being in 5 mutual funds (to get that Couch potato ratio right), when is the right time to pull out given ALL of them are down between 5 and 20% right now? For me to restructure conservatively means walking away with a 10-15% loss on the total book value. Is the right thing to do is suck it up and take that, rather than continue to haemorrage money over the next possible 10-15 years of working life with this company? My only consolation being that the money ‘lost’ was contributed by my company not me?!

FYI, , company DCP is with Sunlife and the mutual funds we are being offered seem to be specifically designed for our company as they don’t offer public information about them on their website. It was hard just researching the 20 odd mutual funds to get ANY information on them. There is no doubt employees of my company are being offered an archaic deal, and in an internal survey last year, I can at least note our employees wanted to have more access to ETFs, more transparency and choice and lower fees in their DCP, but our HR department put it on the backburner :-(

@Cybamuse (and Paul): I hope it’s clear the only thing I’m suggesting is a change to your asset location, not your asset allocation. To use a simple example, let’s say your target asset allocation is 50% bonds and 50% stocks, and you currently have that mix in both your company plan and your self-directed accounts. You may be able to lower your overall cost by instead holding 100% of the bonds in your company plan and 100% of the stocks in your self-directed plan. But your overall mix (and therefore your risk level) doesn’t change.

With that in mind, it doesn’t matter when you sell any specific fund, because you’re going to be buying something similar immediately in the other account. You won’t be buying low and selling high, or vice-versa. You’ll be selling low and buying low, or selling high and buying high.

Within a basic couch potato portfolio, my allocation to bonds is currently 30%, all in XBB. Would you see any need to add any other bond diverisification, or simply stick with the plan and rebalance to my chosen percentages?

Smithson:

Cash, as T-bills, can also actually be quite highly correlated with inflation and can in fact outperform stocks and bonds periodically when inflation is high (but not necessarily after tax – not an issue in TFSAs RSPs RDSPs RESPs). See here: http://www.fpanet.org/journal/CurrentIssue/TableofContents/TreasuryBillsandInflation/

HISAs may be a substitute.

It is a controversial subject. I needed to see the Canada inflation/cash historic relationship for myself because the research is so sparse so I ran some numbers using BofC and StatsCan data comparing the year over year % change in the Canadian CPI with the average of the March, June, Sept and Dec, 90 day Canadian TBill rate from 1974 to 2002. I found the average 90 day T-bill rate exceeds the average CPI over this period by 2.49% which is interesting.

I decided to break down the numbers by the periods of high moderate and low inflation:

Between 1974 and 1983 the average year over year change in CPI was 9.43% and the 90 day T-Bill only exceeded this rate by only 0.13% with several years where the CPI exceeded the T-Bill rate (1974,75,77,79). The TBill rate seemed to lag the CPI for 2 years then catch up then lag again for 3 years.

Between 1984 and 1995 the average year over year change in CPI was 3.48% and the T-Bills exceeded this rate by an average of 4.64%. Perhaps the T-Bill rates were so high because of fears of renewed inflation during economic expansion. This is something to consider given present conditions and historically low rates for the past several years.

Between 1996 and 2002 the CPI average year over year was 1.91% and the T-Bills exceeded by 2.17% on average.

To conclude: in Canada during high inflation the T-bills kept up with inflation, as inflation moderated T-Bills far outperformed and even during low inflation the T-Bills beat inflation, at least as measured by our CPI.

@Colin: It all depends on your time horizon and risk tolerance. If you are comfortable with a 30% allocation to bonds and you have a long time horizon, there is no need for further diversification: XBB is extremely well diversified.

Thanks Dan! I’ll look at my entire portfolio and nut out what I can do going forward. To date I’ve been working to get both company and non-company portfolios to mirror eachother (ie a couch potato portfolio). But in light of the ineptitude of the company DCP, it makes sense to maybe evaluate ALL my portfolio’s instead and allocate accordingly.

Until maybe the markets have a favourable moment and I can completely rebalance across the board without loosing so much. Probably means a bit more active diligence on my behalf for the next few years (as I don’t have much contribution room left in my self-directed RSP and TFSA), but at least I only have to sit down once or twice a year, even with my portfolio not quite in balance, calculate what needs topping up to bring things closer to balancing, and allocate funds accordingly. And then I spend the rest of the year rebalancing by topping up the funds which are out of balance with the couch potato model. I’ll get there…

I’ll get there…. If I wasn’t so in the red from my time before discovering this method, bad timing in general and spending a few years getting more frustrated at mutual funds and their fees and losses before discovering Dan’s wonderful work, I’d rebalance across the board right now! But barring a massive upward tick in the markets which puts everything in the black, I think I’d rather, for now, continue to work towards balancing by topping up my portfolio as and when I have the money available.

@andrew

Thanks for the data! This is something that I’ve always suspected. Larry Swedroe wrote an interesting article looking at the correlation of inflation and different asset classes:

http://www.cbsnews.com/8334-505123_162-57389060/how-to-hedge-against-inflation-hint-forget-gold/

He concluded that the best inflation hedges were T-Bills and TIPS. Of course, TIPS hedge US inflation and as CCP has mentioned Canadian real return bonds options are limited. So this is leading me to conclude that T-Bills are the way to go as an inflation hedge.

Swedroe did his research on one month T-Bills and I noticed that you were looking at 90 day T-Bills. Do you think a slightly shorter duration would improve the correlation?

I agree this is a controversial issue. Even with T-Bills, the best correlation with inflation was 0.55 which is not great. I’m frustrated that I can’t find a product that accurately hedges inflation. You would have thought that the geniuses on Bay Street would have come up with a pure inflation-hedging product by now … (and charge us an outrageous fee for owning it :-)

@Smithson and Andrew: Let’s remember that the goal should be to find an asset class that is correlated with inflation and has an expected real return greater than 0%. I’m not sure T-bills meet the second criterion today, even if they have in the past. 90-day T-bills have delivered negative real returns for four years running.

We can’t predict inflation, but we know the federal government has targeted it at 1% to 3% and has done an excellent job of keeping it there for over 20 years. We also know that 90-day bills currently yield 1%. You can get that up to 1.25% or 1.5% in a high interest savings account. Either way, you’re looking at negative real returns unless we have unexpectedly low inflation.

To Everyone thanks for your suggestions and comments. To CCP – sorry I didn’t mean to hijack a post about Bond ETF’s and make it into something else. Maybe a future article more specifically on this subject would be in order.

I’ve told my work story on line in the past. In 2007 I became more interested in investing. I rebalanced my portfolio just before the crash into “safer” funds offered in our group DCPP. Lucky for me because I personally was not hit as hard as others. I’ve actually done pretty well all things considered. Most of our employee’s however had no idea how to pick their funds as we know these plans tend to be “self serve” for various reasons. Some employees saw the historical return on for example a “science and technology” fund looked really good at that moment so they allocated 100% into it. Surprise when 2008 hit those funds went down 65%. Then of course in typical fashion the panicked uninformed investors sold it all and went into our money market fund 100%. Our money market fund carries a 1.4% mer. So many people did that our provider sent a group letter out explaining that it wasn’t a good idea to keep your funds there because you would lose money as there has been no return on money market funds many years. You simply bleed out 1.4%. It’s been one disappointment after another.

Ive called in many times to the provider, bitched as much as I could, all to no avail. In fact I received sarcasm from some of their staff. In the beginning, I don’t think I asked the right questions as well. My experience was limited.

Value investor : Thanks for your suggestion, I have recently after (4 years of trying) had 2 other providers come in sit with my boss and myself and offer us another alternative. It took quite some time for me to find a provider that works with a 1% or less MER. Some of the people replying here seem to have some decent plans. At least our company is willing to ask some questions. I’ll keep pushing. I will use your last line at the appropriate moment, that’s great.

Dave : You will like this… my employer gives us the full 18%. I have worked here for quite a few years so you can see why losing 2+% every year to fees is no small amount. I’m one of those people who if you run the numbers through an MER fee calculator will have lost a huge amount to fee’s. I can’t see a big name provider like GWL (Power financial daughter) doing something like you mention in your reply. One of my comments to our provider is if they had simply given everyone shares of PWF instead of the funds we are offered , we all be retiring early.

I agree – how can we put pressure on them to reduce fees? Mr. CCP did you attend that OSC meeting in Toronto last week? Fee’s were apparently on the table as a topic. My friends wife is apparently part of FAIR Canada, so I’m awaiting some feedback from her.

I could write a lot more about my “interactions” with our provider – it’s really something but I think the picture is pretty clear already.

@Paul N, Your comments are very interesting. I agree that it would be great if Dan had a topic specifiically regarding investments at company DCPP plans, let’s twist his arm a bit!

My work DCPP plan is absolutely maddening. In our plan the provider reports GROSS performance (before MER’s) and compares this to how well they performed relative to the benchmark index! This is what gets distributed to the employees! Of course they do state that the returns are “gross returns” in the fine print at the bottom of the page, but I’m certain that 99% of our employees don’t realize this.

I’ve also had several run-ins with representatives from the DCPP plan provider. I’ve shown them ETF equivalents (using their own benchmarks) that outperform their own funds for a fraction of the MER. At one point the provider openly admitted to me: “Yes, you’re right, our fees are much higher, but we don’t sell ETF’s and we need to charge higher fees to cover our admin and overhead”. They seem to operate with a certain level of arrogance and impunity since they know that the employees are trapped in the plan and the only recourse is “if you don’t like it, then get out”, which means forfeit the matching company contribution.

I’ve discussed with our company president and he agrees that the fees are too high. However he also claims to be stonewalled by the provider – it seems there are no other viable lower cost options for our company (our DCPP provider is one of the largest in Canada).

Unfortunately it seems we are trapped…very frustrating!!!

@Dave etc: I’m not sure what I could say about group plans that would be useful. Every one is unique, so it would be impossible to be specific. What questions would you like answered?

@CCP,

Sorry for going on about inflation, but it is a subject that I am really concerned about. The reason for this is that I would like to retire as early as possible. Of course, the earlier you retire, the more you are at the mercy of inflation. I would like to believe that inflation will mostly be below 3% in the future, but as you say, no one can predict that. It just throws a serious wrench into my retirement planning.

“What’s happening to my bond ETF” is the exact question I’ve asked myself after logging into my investment account recently. Thanks for this helpful post.

One question then, who or what controls these interest rates which have risen, if they’re not controlled by the BOC lending rate? Are they a reflection of general views on the economy and markets (recently more optimistic therefore rates went higher)?

Thanks again

@Jamie: Longer-term interest rates are largely driven by supply and demand. During times of crisis in the equity markets, for example, investors rush to the perceived safety of government bonds, driving the prices up and yields down. Yields might also go up if investors perceive the debt as riskier than before (though that’s not likely the case with Canadian and US government debt). Investors also demand higher yields if the expect inflation will be higher, etc.

Excellent advice Dan!. Great explanation of what’s happening right now.

So in light of this extremely valuable and informative discussion, and given that I should rebalance this month, does it still make sense to sell some of my equity ETF’s and purchase either XBB or XRB to retain my asset allocation? Would it make more sense to buy GIC’s?

@Trish: I don’t mean to imply that everyone needs to rebalance now. I only meant that you should treat a downturn in the bond market the same way you should treat a downturn in equities: stay the course, stick to your target long-term target allocation, and rebalance when necessary. (That might just mean adding to your bond holdings with new contributions, and not necessarily selling anything.)

Are GICs are part of your long-term plan? If not, I’m not sure why it would make sense adding them now.

I don’t think its one asset class or the other Tbills or Real Returns but a balance according to your long term risk tolerance. I don’t hold cash in RSP in any form. Current yields on TBills may mean a negative real return (TIPS just ticked up to zero yield in the past few days) but according to the data I looked at from 74 to 02 Tbills exceeded CPI by 2.49% on average. I would use a HISA account anyway if its possible because the rates are generally higher than Tbills.

@Dan &/or Others: Could this explain the drastic drop (-10%) over the last month or so in the REITs, or am I missing some other explanation?

Thanks, Que

@Que: REITs and other income-oriented investments (including preferred shares and even utility stocks) are often negatively affected by rising interest rates. But it’s just a correlation: there are other factors that come into play, so some REITs will go down more than others in a rising-rate environment, and a few might go up for unrelated reasons. With bonds, its simple math. When the yield on 10-year government bonds goes up, the price of existing 10-year government bonds goes down by a precise, predictable amount.

http://www.edmontonjournal.com/business/Rate+rise+forecast+pummels+REITs+high+yield+shares/8498163/story.html

I am fortunate in that my pension is 100% employer paid based upon the hours I work during the year and is managed separate from the company I work for. It made 8.35% last year.

The way I look at the drop in bond fund prices is “hey awesome it’s all on sale!! (Same with REITs)”

@CCP informative post as always. In your article you wrote “These days, with virtually all bonds trading at a premium, you should expect the market price of your fund to fall even if interest rates hold steady”. Is this drop in price driven solely by: 1) The fund is holding high coupon bonds (relative today) which are trading at a premium such that the YTM approximately equals today’s interest rates 2) As these bonds mature, they are replaced by lower coupon bonds thereby lowering the average yield of the fund 3) Assuming a constant YTM (constsnt interest rate environment) as the fund yield drops so to must the price? Or am I off base?

Also, when you say “you will not lose money if you hold a bond fund for a period equal to its duration” this is something that has always confused me. I could understand that concept if the bond fund weren’t continuing to buy new bonds. However, since the fund buys bonds as old ones expire, the duration doesn’t tend to change much (not withstanding changes in interest rate environment). So if the duration doesn’t drop aren’t you continuing to be exposed to interest rate risk for the new bonds that are purchased. So if a funds duration is 7 years and you purchase it today and hold it for 7 years, how do these new bond purchases within not have an impact?

@Paul N

I’m not sure if there is considerable overhead for running a DCPP versus a Group RRSP, but I know that GWL is capable of much better than what they are giving to you. My employer has a Group RRSP through Great West Life, and they at least offer four index funds that would replicate the global couch potato model portfolio for less than the cost of Option #3 on Dan’s model portfolio page.

At some point, I believe it is the responsibility of your employer to negotiate better fund options. I doubt that GWL will change the funds offered because of one unhappy employee at a company whose DCPP they manage when they are making money hand over fist off of you. Instead, you might have better luck with your human resources department – perhaps you could explain why fees matter and have your company use their leverage to provide better funds, or take their pension somewhere else.

The index funds I have access to through GWL (with fund code and MER) are:

TDAM Canadian Equity Index Fund – S120 – MER 0.681%

TDAM U.S. Equity Index Fund – LUSET – MER 0.686%

TDAM International Equity Index Fund – LIEIT – MER 0.707%

TDAM Canadian Bond Index Fund – S079 – MER 0.676%

@Adam: if a bond has a YTM of 1% but a coupon of 4%, the difference has to be made up by the price falling along the way. As usual the market is an excellent system for adjusting the price daily.

@B/Paul: The posts about “MERQ” at Michael James on Money are a great way to look at fees. Why talk about 1-2% when you can show how it’s costing 25-50%?

TD Index funds are indeed among the best of the worst. I’m currently seeing them in a Sun Life plan. I can’t remember what options were in the GWL plan it replaced but I think a few were similar.

@Adam: To answer your first question, as Value Indexer points out, the price drop comes from the capital loss that occurs when a premium bond matures. Technically bonds never mature in an ETF: they are typically sold when they have one year remaining to maturity. But the effect is still the same.

Your second question about duration is pretty complicated. If understand correctly, you’re observing that if you buy a 10-year bond with a duration of seven and hold it for two years, you will end up with an eight-year bond with a lower duration. But if you buy a bond ETF with an average term of 10 years and a duration of seven, then after two years the ETF will still have an average term of 10 years and a duration of seven.

That’s true if rates don’t move. But with a bond ETF, the turnover in the portfolio means that all interest payments are reinvested in higher-yielding bonds when rates rise. In that environment, the higher coupons would shorten the duration of the fund. All of the illustrations I’ve seen make it clear that bond funds tend to recover relatively quickly from interest rate increases precisely because of this feature.

Duration is just an estimate, not a precise number. But it is safe to say that money invested today in a broad-based bond with duration of six won’t suffer a loss over a six-year period because of interest rate increases. The take-home message is that people with a 20-year time horizon probably shouldn’t be holding only short-term bond ETFs because they’re worried about price declines in the next year or two.

While it’s true that a bond fund could lose money continually if interest rates rose every year, that is unlikely to happen over an extended period. I also suspect it would take rapidly accelerating rates to make this happen since you would be collecting a higher yield every year which makes the duration shorter. That’s about as likely as the $200 oil targets that were being thrown around in 2008.

B: Thank you for your comments and advice. Information like that is great – I’m doing my best to get the right people informed here. I will do some cut and paste with your notes here.

VI : I Have used Michaels calculator. When we had our lunch meeting’s with two alternative providers I presented my argument using that tool. In fact I have used articles from Bloggers, Moneysense, Canadian Moneysaver, Rick Ferri, and so on. I also like Steadyhand’s structure where the fees are reasonable to start and they drop as your portfolio’s value increases. They however do not offer group plans. Also our CEO is very “analytical”, after reminding him several times to try the calculator he finally did. As I have said this is a long process and I think many of us who take the time to sign up on a website like this one or Michael’s “get it”. Unfortunately there is very few of us. I can’t understand how people can just brush off losing a large portion of their retirement money.

People tend to listen to a fast talking financial salesperson wearing an Armani suit, not the middle manager wearing a polo shirt. You can imagine in the background the BS machine is churning from GWL telling our person in charge all the cliché lines to continue to “sell” their overpriced plan.

A bond ladder “catches up” in an environment of rising rates.

Is this also true of a bond ladder ETF?

@John: Yes, the same idea applies with a laddered bond ETF. Every year one rung of the ladder is sold (when the bonds reach one year to maturity) and the proceeds are reinvested at the longest maturity, so in a rising rate environment the YTM on the fund would gradually creep up.