The mutual fund industry loves to sell past performance, and it’s not above massaging the data to make that performance look even better. But every now and then an advertisement appears that sets the bar even lower. Michael Callahan, a financial planner in Ottawa, recently sent me an ad for IA Clarington Investments that might be the worst one I’ve seen yet. “I figured you might welcome an opportunity to rip this one to shreds,” he wrote. Challenge accepted.

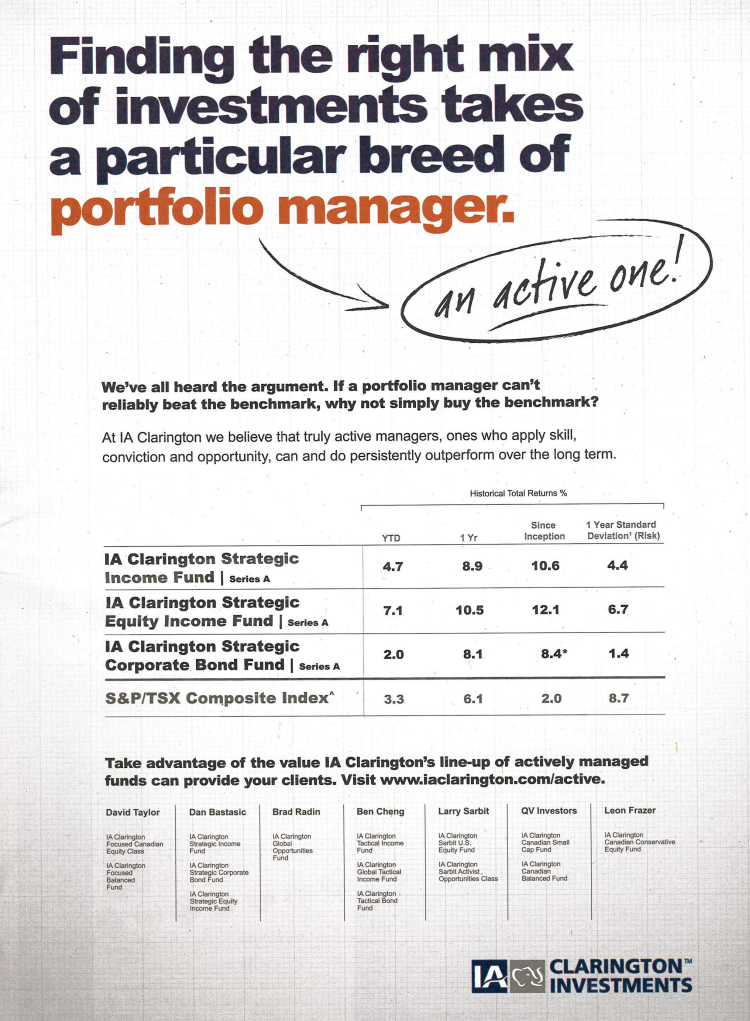

First there’s the time frame. The ad says the company believes active managers “can and do persistently outperform over the long-term.” But as explained in the fine print (microscope not provided), the year-to-date returns in the first column of the table are for the period ending March 31, so we’re talking about three months. We get 12-month returns in the second column, and the third column gives the funds’ returns since their inception. Problem is, the three funds spotlighted here were launched in the late summer of 2011, so they had been around for all of 18 to 19 months when these returns were calculated. That might be long-term if you’re an insect, but for the rest of us, it’s an utterly meaningless time frame for assessing investment returns.

First there’s the time frame. The ad says the company believes active managers “can and do persistently outperform over the long-term.” But as explained in the fine print (microscope not provided), the year-to-date returns in the first column of the table are for the period ending March 31, so we’re talking about three months. We get 12-month returns in the second column, and the third column gives the funds’ returns since their inception. Problem is, the three funds spotlighted here were launched in the late summer of 2011, so they had been around for all of 18 to 19 months when these returns were calculated. That might be long-term if you’re an insect, but for the rest of us, it’s an utterly meaningless time frame for assessing investment returns.

But we’re just getting started. The funds’ returns are compared against the S&P/TSX Composite Index, the traditional benchmark for Canadian equity funds. But none of the funds in the ad fall into that category. The IA Clarington Strategic Equity Income Fund comes closest with 63% of its holdings in Canadian stocks, but it also includes 21% US stocks. The IA Clarington Strategic Income Fund is 38% Canadian equities, 14% US equities and 32% fixed income. Meanwhile, the IA Clarington Corporate Bond Fund includes precisely zero Canadian equities: it’s a high-yield bond fund. (The fine print does state that the benchmark index contains no fixed income, but acknowledging that doesn’t make the comparison any less worthless.)

So here’s an ad arguing that skilled active managers can outperform their benchmark over the long term, and the “evidence” covers an absurdly short period and uses an entirely inappropriate benchmark. It’s like they weren’t even trying.

What makes the ad even more outrageous is it appeared in an industry publication, so its target audience is advisors. We’re used to the fund industry being contemptuous of retail investors, but one would hope even the dimmest advisor would see through such obviously fatuous claims.

What the evidence really shows

Let’s consider IA Clarington’s claims using more meaningful data. Since we’re looking for long-term outperformance compared with the S&P/TSX Composite Index, we’ll go out a wee bit further than 19 months and we’ll consider funds that actually hold Canadian stocks. The IA Clarington website lists four that can be meaningfully compared to a broad-market index (89% to 98% of their holdings are Canadian equities), and all of them have a track record of at least 10 years.

Here’s what the returns of those funds look like compared with the iShares S&P/TSX Capped Composite (XIC). Market-beating returns appear in green.

| Fund | 3-Year | 5-Year | 10-Year |

|---|---|---|---|

| IA Clarington Canadian Dividend A | 5.75% | 9.09% | 5.58% |

| IA Clarington Canadian Growth Series A | 2.03% | 8.52% | 5.10% |

| IA Clarington Canadian Leaders | –0.13% | 5.47% | 5.91% |

| IA Clarington Canadian Conservative Equity | 6.03% | 8.79% | 6.98% |

| iShares S&P/TSX Capped Composite (XIC) | 3.57% | 9.76% | 8.16% |

Annualized returns as of November 8, 2013. Source: Morningstar

Interesting how the story changes when you actually make a fair comparison. It might be true that active managers “who apply skill, conviction opportunity can and do persistently outperform over the long term.” Unfortunately there is no evidence of this in any of IA Clarington’s Canadian equity funds.

“We’ve all heard the argument,” says the first line in the ad. “If a portfolio manager can’t reliably beat the benchmark, why not simply buy the benchmark?” Why not indeed.

You still give them too much credit by comparing their dividend fund to XIC. The 3-year annualized return for XDV is more than 9.79% (5 year is 11.54% and 10 year is 7.92). Same can be said for their Conservative Equity fund.

I still don’t understand how the majority of Canadians will go far out of their way to save a buck but have no idea how much they are wasting on their managed mutual funds and are too intimidated to ask.

Oh they were definitely trying. It just goes to show how amazingly deceptive we allow these companies to be. I see ads like this all the time that compare the performance of the company’s bond fund to the S&P 500 over the past X years, and it’s disgraceful. Most people won’t know why that’s meaningless. We really should have standards that prevent this kind of thing.

@Matt: There are regulations about how mutual funds can advertise their performance, and regarding the comparison of fund performance to appropriate benchmarks.

http://www.osc.gov.on.ca/en/SecuritiesLaw_sn_20130718_81-720_rpt-cd-review-sales-comm.htm

But as this ad shows, you can bury the important info in the small print and few will ever read it.

Another common trick is to compare the fund to a price-only index that does not include reinvested dividends. That always makes a fund look far better. In this case, IA Clarington did not do that, to their credit.

I think this too is pretty shocking and speaks for itself :

Mgmt Expense Ratio (MER): 2.77%

OMG do people still invest in funds at that rate? Please everyone wake up!

Run that through Preet’s long term investment calculator and watch your money burn…

@Paul N: I think it’s interesting that the dividend yield on the S&P/TSX Composite right now is about 2.7%. That means investors in funds like this are essentially forfeiting 100% of the dividends in fees. You can also find examples of bond funds where the fee is approximately equal to the yield. I guess you better have high hopes for capital appreciation if you’re investing in these things.

As for how many people still invest this way, the four funds listed above have a total of $2 billion in assets, combined with $1.36 billion for XIC.

Thanks for Sharing CCP.

I wanted to Thank you for opening my eyes to the Couch Potato Investing btw. Me and my wife love it. Presently , we have over 150 000 k invested in the complete couch potato portfolio and We CAN SLEEP AT NIGHT.

Those Mutual Funds straight up, are stealing your money. As my wife says… “Crooks in Suits.”

no offense to anyone and Have a nice Remembrance day.

Another great article highlighting that we, couch potato investors, are on an excellent path!

Hey Dan .. Love this one… Clarington has a long history of deceptive marketing . Readers should also look into which other companies they are associated with. They are well known by regulatory bodies like obsi. Great work exposing the truth

Hi CCP:

Regarding the returns of the Clarington Funds given above..Are they net of MER/TER and Tax? Tax bleed should be high as the turnover on these mutual funds are astronomical.

thanks

Prasanna

@Prasanna: Mutual fund performance is always reported after fees, but before taxes, since taxes will vary among individual investors.

““We’ve all heard the argument,” says the first line in the ad. “If a portfolio manager can’t reliably beat the benchmark, why not simply buy the benchmark?” Why not indeed.”

I can feel the heat of that burn from here :) Oh, snap!

Just like my recent Tweet for this post… #thetruthisoutthere.

Nicely done Dan. Glad I stopped investing in mutual funds a long time ago.

I need to kick my dividend stock habit eventually but that’s going to take much more work. :)

Mark

Simple logic says that if an active manager had a consistent winner fund, they would only recommend that one fund. But a simple screen shows that they currently 105 different domestic stock mutual funds. Why? There are only 60 big stocks in the TSX 60. It’s not just IA, there are over 5000 domestic stock mutual funds. Again there are only about 250 sufficiently liquid stocks in Canada.

My view is, if any mutual fund company has more than one fund, it’s a sure sign that they don’t believe in their manager(s) so why should I believe in them.

But the worst one are segregated funds… they charge huge MER even on MM funds. recently I came across SSQ Investment and Retirement company.

Example of their funds:

Canadian Index : MER between 2.76 and 5.26%!

https://investissement.ssq.ca/astran…achetable.html

They offer GIC , amount up to 10K

1y – 0.65 , 2y-1.00, 3y- 1.35, 4y – 1.70, 5y- 2.05

Example of their funds:

Canadian Index : MER between 2.76 and 5.26%!

I just cannot get how such companies are surviving and who are the “idiots” who invest there?!

IA Clarington has a knack of hiring washed up , has been money managers. David Taylor blew up Dynamic, Larry Sarbit market timed himself out of a job at Investors Group and Ben Cheng’s company is essentially bankrupt (TSX – AHF) . The game changes next year when commission rules show people how much money everyone in the machine steals from their savings.

@gibor – I love their (SSQ) slogan “we thrive on mutual trust”. It seems they certainly do!

I’m not sure though if picking on “specific” companies here is really helpful. We can go down a huge list of bad actors. This subject has been a real sore point with me for years since I have started investing. I personally know people that have been “taken” by various MF sellers. Front load fees – Crazy MER’s – Rear load fee’s – for seven years ! One company that even has an hour radio show on an AM station in Toronto on weekends – touting they are “different”. When you actually sit down with them and talk products + numbers – turns out they are exactly the same as any other and a subsidiary of a big name Fund company. Just a different spin to get your attn.

IMO this subject gives the whole industry a bad rap. The good companies should distance themselves from the bad and make sure they get that message out clearly. The industry across the spectrum needs severe changes. I don’t want to walk into another Tim Hortons and see some unfortunate person signing papers with Prime America or WFG with a leverage loan they can’t afford to be in to boot, and think he is getting the best return for the little money he/she makes. It’s simply sad and disgusting.

I felt sometimes I was really alone in complaining about this. It’s really refreshing to see all these comments. I think finally we are getting somewhere. I repeat myself here from comments I have made on other blogs. Yes I understand – charge some fee’s but let’s all be fair and reasonable. $350,000.00+ lost in fee’s that some family has contributed to over a lifetime (in simple high fee funds) that has amassed about a million dollars. That is not fair! That’s my rant for today….

@PaulN I agree that it’s a industry and country wide problem… but it is clear that it is no mistake, it’s all by design to extract as much money as possible from lay people. Things that bug me about the industry:

MF sellers are called “investment advisors” – truth is, they are sales people with no fiduciary duty. This terminology “advisor” should be outlawed for anyone that does not have a fiduciary duty.

MF advertise MER’s wrt assets which does sound too bad to the lay person – truth is, when to look at them wrt to returns, you realize they can often be taking the majority of the return. It’s even worse when you realize they’ve taken no risk. This should be made more clear to investors via standardized reporting.

Vast majority of MF’s cannot beat an indexed portfolio.

Canada has some of the highest MF MER’s in developed world. Canada should allow more foreign players in.

Industry can “kill” and hide old mutual funds that didn’t perform so they can advertise with a selection bias. Regulators should force that all historical data be easily and freely available to investors so they can see a company’s true track record.

Industry can compare their fund to anything. Should only be able to compare to meaningful indexed benchmarks.

Most people’s MF statements don’t list personal rate of return and compare it to a meaningful indexed portfolio. I’ve seen many statements that are intentionally misleading and/or hard to read. A clear personal rate of return should be mandated, so that a lay person can see how their MF portfolio is performing. (Easy to do in today’s computer age.)

All fee’s should be made transparent. Back and front-end fees should be outlawed as anti-competitive because of the lock in effect and because of their historical abuse with un-savvy investors.

Licensing of “investment advisors” is a joke because they clearly the rules in place don’t make anyone look out for investors. So scrap it and make everybody know that it didn’t work and that it’s really a caveat emptor situation.

But I won’t hold be breath for any of this to get fixed.. too much power and money involved.

Most deceptive investment ad I ever saw was in Australia in 1997 and was paid for by the Australian Real Estate people proving that real estate was a far better investment than shares. The time frame chosen was the 10 year period ending the month the ad was published around September/October of that year. Think about it. 10 years before 1997? Yes, they chose the time frame to coincide exactly with the peak of the market in 1987 just before the October crash.

Worst reporting of the year?

Dan I do agree that the add is misleading however what’s ironic about all this is that YOUR comparison of ETF vs. those funds is also misleading. Unless you are a DIY investor do you really think an advisor is going to sell ETFs for free? In many cases advisor change clients more when they use ETFs and as result make more money off clients. It’s a dirty little secret that is going on in the industry. Case and point take a look that the link below:

http://m.theglobeandmail.com/globe-investor/personal-finance/etfs-spurring-shift-to-fee-based-advice/article545003/?service=mobile

He even admits to charging 1.40%!!! The is making even more money off his clients over the 1% fee he would have been paid by the fund co. Why don’t you redo your ETF comparison again factoring in the whopping 1.4% annual fee this advisor charges so we can then see how the mutual funds with the embedded 1% compensation stack up. Or better yet just use a Fee based version of the funds.

For the record I own MFs, ETF, and stocks.

Thanks!

@Allison: This is an age-old debate and it can be exhausting, but I will just make one point. You are assuming an advisor’s role is to help a client beat the market after fees. I would argue an advisor’s role is to add value by providing services that help the client earn a higher return after fees than he or she would have been able to achieve on his or own. Those are two very different things.

I have always advocated do-it-yourself investing for those who are capable of it: there is no point in paying for advice you don’t need—or as is the case with many mutual fund salespeople, “advice” you’re not getting.

@Alison, let’s run the numbers for an apples to apples comparison of IA Clarington Canadian Dividend MF vs. iShares

Dividend Aristocrats (CDZ). Let’s assume $500k initial investment, a client who needs advice, trailing 5 years to Oct 31,2013, 2% FE load for IA MF (which is a load fund that can actually charge up to 5% FE) and no yearly advisor fee vs. 1%/yr fee-based advisor. Annualized total returns were 9.1% and 12.4% respectively. After all advisor and sales fees, the final results the investor would see:

IA Dividend MF $754k

iShares Dividend ETF $858k

So, the “whopping” fee-based ETF index advisor just improved her/his clients return by $104k over the “free” MF advisor. A DIYer would be even better off, but I assumed a neophyte.

Sources: I used iTrade/Morningstar and iShares sites to get 5 years returns.

Lets not lose perspective of my original comments. Your comparison of an ETF with zero commission charge to a mutal fund with embedded service fee of 1% is equally as bad as the IA marketing piece!

Brian, this is not about MF vs ETF’s. I own stocks, ETF’s and MF’s so I am impartial. The point was if you are going to toss up performance on this blog make sure you compare apples to apples.

For the record both of these F series funds beat their respective indices.

https://secure.globeadvisor.com/gi/db/gaf.fund_pro?fundname=IA+Clarington+Canadian+Dividend-F&pi_universe=PUBLIC_FUND

https://secure.globeadvisor.com/gi/db/gaf.fund_pro?fundname=IA+Clarington+Cdn+Conservative+Eq-F&pi_universe=PUBLIC_FUND

@Allison, I sincerely don’t understand what you mean. My comparison were all costs included in both cases. It’s apples to apples.

Brian, I’m sorry you don’t understand. I don’t know else how communicate this to you?

Take care,

Allison

@Allison, it’s not good form to make extraordinary claims and then not back them with anything and just arguing.

But just ensure to everyone that reads this blog that I am not making things up, I will attempt one last time to show that this is apples to apples and again I will give sources.

CDZ has an embedded MER of 0.66%, the fee-based advisor in your linked article charges an addition 1%. That makes the total annual fee to the investor about 1.66% and the advisor gets 1% and Blackrock gets 0.66%.

IA Clarington Canadian Dividend Fund has an embedded MER of 2.77% which is the total annual fee to the investor. The mutual fund advisor will get an annual trailing fee from this MER of 1% and IA gets 1.77%. Additionally, at purchase the investor will be charged up to 5% FE load/sales commission which all goes to the advisor. In simple terms this is called extracting as much money as possible from the poor investor.

If that’s not bad enough for the poor neophyte investor. Here’s another worry, it seems that IA was making unsustainable payments that has eroded the capital. http://thewealthsteward.com/2013/05/this-fund-is-unlikely-to-sustain-its-newly-lowered-monthly-payout/

Sources: iShares website, IA Clarington Investments Inc. Simplified Prospectus June 10, 2013

The real underlying problem is not the industry, it is with a large segment of individual investors. I know so many people that will drive extra miles to save 2 cents per liter on gas but can’t seem to find more than 2 minutes of their time to look at their investments. If people refuse to educate themselves, it’s only fair that they pay the price of their stupidity.

It’s like going to a car dealership without have any criteria. You can’t blame a salesmen selling his most profitable product.

Linda, not exactly… “advisors” frequently lying, ot better to say – hiding information about MER, fees, performance etc…. and you cannot hide facts when you selling your home or you will be in trouble…

Majority MF investors just have no idea that they are robbed…

Allison, you wrote “For the record both of these F series funds beat their respective indices.”…I don’t know what you are talking about and what indexes they compated to… I just compared performance of IA Clarington Canadian Dividend vs CDZ (dividend fund vs dividend ETF). 5 years return:

IA – about 40%

CDZ -about 80%

Yield on IA – 0.24%

CDZ – 3.2%

Nothing even to compare.

P.S. I don’t think CDZ is a perfect investment. I prefer to hold individual stocks …but still , it’s much better than MF

@Linda

There is so much wrong with what you have written just above. In a nutshell you say it’s ok to screw someone over that is ignorant about investing. It’s because of people like you we need a fiduciary standard rather then our ridiculous “suitability standard”.

Do you think everyone can spend time and understand the complex world of investing? Maybe everyone should learn how to build their own cars or build their own house too? If their “too stupid” as you say to do those things too, I guess we all should be “taken” by those who can? Your argument is ridiculous.

Your exactly the reason we try to invest on our own rather with anyone with an attitude like yours. If you are really some kind of advisor I feel sorry for your clients. (Victims is probably a better term for them).

Please find another profession.

@gibor: The first rule is not listen to what advisors say and look at what the contract says. These fees are detailed somewhere in the contract. It’s no different from cell phone or insurance contracts that people sign without reading them first.

@Linda, I’ve never have advisor and won;t have in future… I spoke with some advisors and after some questions I asked, I cleary understood that thay know even much less than me… :)

I just read some books and many blogs, websites like seekingalpha.com , opened discount brokarage accounts and started to invest by myself… I have mixed of invividual stocks CAD and US (mostly blue chips paying dividends for many years) and some ETFs. MF I hold practically only in RESP which I don’t want to move to discount brokarage… the only exception …I hold a little bit TD mutual funds, mostly eSeries with very low MER.

As per your advise about reading contracts….you know , those contracts are very difficult to understand , it’s not a simple “language” and you probably need lawyer to explain you everything… imho, it’s much easier to understand basic investment skills, like with coach potato examples, than understand those “advisors” contracts.

P.S. In any case, I beleive that MF, Seg funds etc is a dying industry. My son this years graduated from high school and started university… in high school they had investment classes and studied a lot of advanced stuff include not only basic investments, but also naked puts, batterfly spread and so on … and I;m 100% sure that no one from his class won’t touch MF in their life… and other delinquents just don’t invest, hundreds thousands of immigrants (and I;m one of them), also not so stupid to waste money on useless advisors….so this is mostly an old generation who holds MF

@Paul N, imho , everything should be disclosed …. all MERs , fees , admin charges, DSC charges (the most ridiculous thing ever) etc… everything should appear in statements… I’m pretty sure that majority of MF investors don’t have any idea what they are paying…

I hate the most segregated funds with their relly ridiculous MERs even on Money market funds and promisses of getting back 75% of guarantee after 10 years! They never mention how many times in history any index was down 25% in 10 rolling years! (it’s never) and that those 75% are not linked to inflation.

imo the governmenet should imply stricter rules regarding all those so called “mutual” funds

@Linda wrote “If people refuse to educate themselves, it’s only fair that they pay the price of their stupidity.”

WOW!!!! I can’t believe you said that in a public forum, but I think it summarizes the contempt the MF industry feels for their clients. This why I argue that MF “advisors” should really be called salespeople and be refused the right to lie and call themselves advisors.

I ask if you were the investment “advisor” for a disabled person (e.g. has Alzheimer’s, mentally handicapped, etc.) then you would feel fine taking their money and having them pay the price of their stupidity.

I happen to have a person with Alzheimer’s in my extended family that I have to watch out for because we’ve had MF agents like you among others tried to rip her off. Luckily we’ve got power of attorney now and are going after these people…

I did a quick analysis on the effect MERs have on the pension income of a retiree. If you compare John and Paul. Both are 30 years old and will retire at 60. They both invest $500/month to retirement then they will consume their savings during 30 years of retirement. Market returns are 6%. John invest in mutual funds with an average MER of 2% and net returns after fees of 4%. Paul is a DIY investor and invest at minimal fees assume 0% for a return of 6%. Paul will receive $3,000/month for a total of $1,083,000. John will receive $1,660/month for a total $596,000. John has lost about $500,000 in retirement income, all to pay fees. The mutual fund company did not invest any money nor did they take any risks and they collected $400,000 to $500,000 in fees. What a beautiful business to be in. What did they do for these fees? A couple of hours every to re-balance and calling the client at RRSP time? And our pension experts are worried that our pensioners will run out of money. They may find the solution in the investment industry’s pocket. Our government who is appointed to protect its citizens, have the audacity to invite members of the investment industry to help them solve the impending pension crisis. The solution is very simple – look at what the UK and Australia did to put the brakes on this incredible deception and the exploitation of the uneducated seniors.

Hilarious. Unfortunately, 99% of those who read that ad copy don’t have the financial background to see through the hype. That’s a win for a marketer.

@Gerry Makes you a little crazy once you know the game is rigged, eh?

I know this goes again the indexing approach of this blog but my suggestion is if you can’t beat them join them and just buy some bank stocks for your portfolio. In my opinion, that’s much more likely to be profitable than investing money in any mutual fund the banks sells.

P.S. Don’t buy a Financials ETF… MER is too high for the few stocks it holds.